Close menu

- Home

- News

- Insights

-

Digital editions

- Back to parent navigation item

- Digital editions

- 2025 digital editions

- 2024 digital editions

- 2023 digital editions

- 2022 digital editions

- 2021 digital editions

- 2020 digital editions

- 2019 digital editions

- 2018 digital editions

- 2017 digital editions

- 2016 digital editions

- 2015 digital editions

- 2014 digital editions

- 2013 digital editions

- 2012 digital editions

- 2011 digital editions

- 2010 digital editions

- 2009 digital editions

- 2008 digital editions

- 2007 digital editions

- Awards

- Conference

- Advertise

- Training

- Cappro

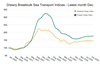

Drewry’s Breakbulk Sea Transport indices

By David Kershaw2025-01-15T16:14:00

Source: Drewry Multipurpose Shipping Forecaster

Drewry has published its latest Breakbulk Sea Transport Indices, which track both the project and general cargo shipping sectors.

Already have an account? LOG IN

To continue…

Keep up to date on the latest information on over-dimensional and heavy cargoes.

Enjoy free unlimited access to HLPFI news, and receive our 2 weekly newsletters

Follow Heavy Lift & Project Forwarding International on social media

- Terms & Conditions

- Cookie Policy

- Privacy Policy

- Advertising Terms & Conditions

- Archive (by date)

- © Heavy Lift & Project Forwarding International

© DVV Media International Limited

Site powered by Webvision Cloud